In this article, we provide some background on the need to diversify among asset classes then demonstrate a conservative portfolio which produced significantly better risk-adjusted returns than the S&P 500, and finally discuss current issues related to the COVID-19 situation. The intention of this article is to shed light on the importance of multi asset class diversification; we do not recommend or endorse the portfolio demonstrated.

BACKGROUND

- Inflation: which is impacted by printing of money among other things

- Interest rates: which is decided by central banks based on economic, political and social factors

- GDP Growth: which sometimes turns negative leading to recessions

To demonstrate the need for a multi asset class portfolio, each of the mentioned dimensions are listed below along with an example of an asset class that is highly impacted by it. Since we don’t know future actions and expectations that can impact inflation, interest rates and/or GDP growth rates, there is no way to rely on a single asset class to capture some of the upside and be reasonably protected from the potential downside of unknown economic changes.

Inflation Impact on Gold

GDP Growth Impact on Stocks

As you can see, stock values generally follow the trend of the economy with sharp declines during recession periods (i.e. the 2000 Dotcom Bubble and 2008 financial crisis); it is worth mentioning that it took about 25 years for the index to recover from the sharp decline that happened in 1929 at the start of the Great Depression.

For full S&P 500 historical trend, you can check https://www.linkedin.com/pulse/navigating-covid-19-through-time-diversification-mohamed-rafea/)

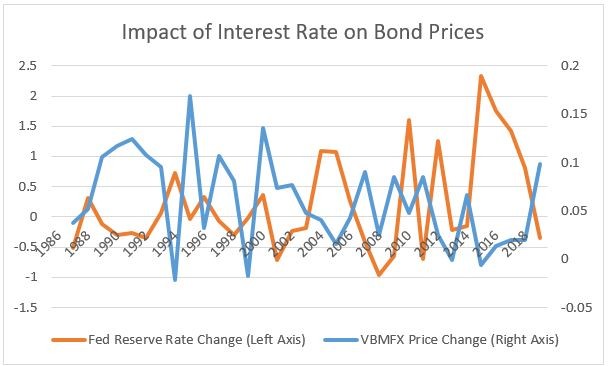

Interest Rates Impact on Bonds

Bond prices are highly sensitive to changing interest rates. Below graph shows percentage changes in the Federal funds rate along with percentage changes in the adjusted close prices for Vanguard Total Bond Market Index Fund Investor Shares (VBMFX) which “invests about 30% in corporate bonds and 70% in U.S. government bonds of all maturities (short-, intermediate-, and long-term issues)”

More fund details can be found at

https://investor.vanguard.com/mutual-funds/profile/VBMFX

PORTFOLIO

- 55% in a security tracking the VBMFX index

- 30% in a security tracking the S&P 500 index

- 15% in Gold

COVID-19 SITUATION

Amid the current COVID-19 pandemic, multiple economic dimensions experience a great deal of uncertainty. We are entering a recession that no one knows when it will end. Money supply increased dramatically due to Federal Reserve actions (some details can be found in https://www.usatoday.com/in-depth/news/2020/05/08/national-debt-how-much-could-coronavirus-cost-america/3051559001/). The Federal Reserve is buying assets with trillions of dollars almost doubling its asset ownership in its balance sheet. Interest rates are almost Zero making them an ineffective tool to stimulate the economy.